If you've been following The Depot, you'll know that Lunexus is focused on creating the still nascent ecosystem to provide hardware to the only existing customers in space so far: the fast growing satellite market in LEO (Low Earth Orbit). Even with the many brilliant people working in the space industry, and even within ISAM*, we often have difficulty in conveying our reasoning on WHY this is so important, but also HOW it can be feasibly done. We are typically met with a great deal of skepticism on the feasibility front.

In-space Servicing Assembly and Manufacturing (ISAM) is a term that has emerged from the space industry, eclipsing other acronyms like OSAM (Orbital SAM) to be more inclusive of the Lunies and Martians. There's an entire lava tube rabbit hole of why/how this came about, but suffice it to say it's an attempt to jump on the Artemis funding bandwagon.

*ISAM vs. OSAM

Being able to cogently express both the why and the how is critical for Lunexus to find both investors and government funding sponsors (strategic customers).

Beginning with Why

Although it took 80 years since sputnik to get this point, we as a civilization now have a commercial ecosystem in LEO. It's no longer solely the province of nations. Recent estimates say that the space industry is now worth over $600B and will hit $1T by the end of the decade (this estimate probably leaves out inflation).

These big dollar numbers might be enough "why" for you, but in the startup world, it's critical to understand your market and your customers within it. You also need to understand the ecosystem (value chain) of that market.

Humanity is furiously deploying satellites into orbit at an increasing rate. This is a demand signal beyond the dollars. Despite the hype, the demand isn't for more launches; it's for more satellite capabilities, primarily from what I call the infosat sector: communications satellites, navigation satellites, and Earth observation satellites (including weather sats). They all have the same model: Deploy hardware (cost), and send down data (revenue).

The value chain is everything that goes into that cost and affects revenue. The circular economics world also has a way of looking at value chains. It's called a Life Cycle Assessment (LCA) Inventory. Conventionally, it's depicted with a Sankey chart emphasizing the material flow from each process to the next, from cradle to grave. The width of each node is proportional to the flows.

Please allow me to make an introduction: Circular economists, meet space entrepreneurs.

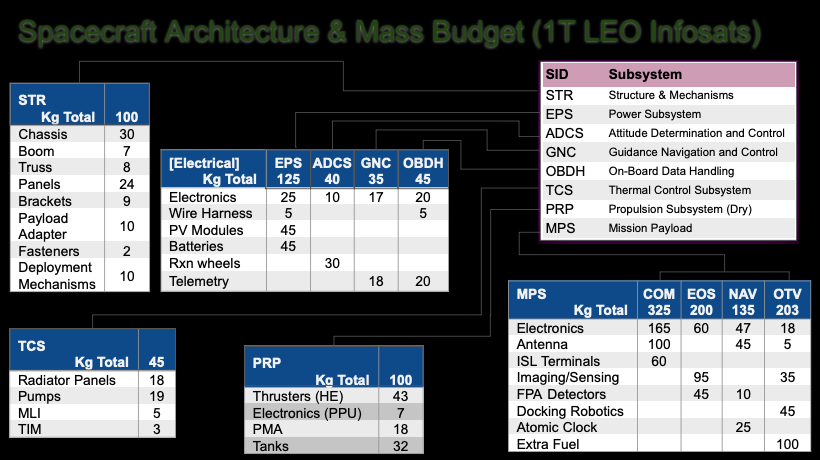

I've spent the last couple months building the satellite model for this using a notional 1,000 kg (1 tonne wet mass) communications satellite. Altering convention, I've pointed the flow upwards because space nerds aim for the stars and also the text works better that way. In this draft version there is still some mass balancing and color coding to be done, but there's enough to show the gist of what a typical satellite requires. Note that I've vastly simplified this model to keep it from being complete spaghetti, so apologies if I've left out your pet process. It's still plenty complex. I've also broken down the process stages into eight bands that not only encompass both ISRU and ISAM, but also the Operations stage where we realize the full value, and the End of Life (EOL) stage where we see what ultimately happens to our resources.

Right out of the box, we can see that more than two thirds of what goes into deploying a satellite is launch fuel that gets blasted out the backside of the launch rocket. We are assuming a completely reusable launch system, so the rocket mass itself isn't even shown here, and the fuel mass is normalized to a 60 satellite payload. We also are neglecting the LOx (liquid oxygen) mass, so it's really even worse. We won't even discuss ground support.

Such is the tyranny of the rocket equation. This, right here, is WHY it's rational to make satellites in orbit to the maximum extent we can. Imagine any product that could reduce its material by 70%. Now imagine it's a product that's doubling demand every two years.

Now, the How...

The beauty of this chart is that it also gives us "the how". The 80 or so nodes on this chart each describe a technological process for adding value to materiel all the way from ore to satellite. These processes are currently all done on Earth (at least up to Stage 6). If we want to build a satellite in orbit, we have to translate enough of these processes to the microgravity vacuum domain and connect them commercially and logistically.

This is a strategic development roadmap.

No argument: it's a big buffalo- too big for even the largest conglomerate. Not even SpaceX, the poster child of vertical integration, mines and refines its own raw materials, or fabricates MLI, silicon PV wafers, and optical sensors.

This cannot be done by a single entity. That's actually a good thing, because multiple competing entities create better resilience than relying on a single point of failure. The challenge is in technology integration and cost. Standards and coordinations are needed to ensure interoperability. As a recent case study, Starliner's ISS mission snafus highlighted the inconvenience of crew suit compatibility with Dragon architecture, resulting in an extended stay for Butch and Suni. Although Boeing caught most of the flack for this, the responsibility for this incompatibility was at the NASA program level.

Someone needs to coordinate. Some would argue that this is a role for government. Some would counter that it should be done by trade organizations. In the ISAM community, we have two such trade orgs: CONFERS and COSMIC. Lunexus is active in both. CONFERS is an international organization more explicitly focused on servicing (the "S" in ISAM); COSMIC is a US specific entity with a more holistic approach to ISAM. However, neither of these provide funding for strategic technology development.

If we select any single node on this chart and solve the technical challenges to plop it into the orbital domain, we immediately have a commercial viability issue: by itself, that node has no customers and no suppliers. Generally speaking, smart investors like to see customers for sure, and smarter investors like to also see a supply chain. If you have neither suppliers nor customers, you have to find investors with both vision and high tolerance for risk (there are no dumb investors, not for long at least). Venture capitalists as a rule like to see returns inside 5-10 years, so strategic space hard tech development is a tough sell for VCs. This is why we typically go first to non dilutive government grants. There has been a troubling trend of these grant programs to try to measure their success like VC's, and an even more troubling trend of questioning their very need. VC funding and non dilutive government grants are not interchangeable.

But let's say we solve the funding problem using either strategic government vision or private investment that can chain together enough ventures to produce something functional. Let's say we get enough ventures that can successfully integrate enough processes to sustainably turn a profit for themselves. What portion of this technology stack roadmap do we need in orbit for any of it to compete with making satellites on the ground and launching them? This begins to sound like an optimization problem.

I have somewhat arbitrarily set what I think is an achievable goal that we should be able to make 50% of a satellite from orbital materiel. 40% of a typical satellite is aluminum, which is already the easiest thing on Earth to recycle. This was the approach of our first award from the 2022 NASA Orbital Alchemy Challenge for the Arachne+WEB proposal. There are other people also working on this approach; the OSAM-2 program was supposed to demonstrate using aluminum to 3D print a truss, but has been cancelled with no replacement demo in sight. Our second award was for the Arachne+SiLK approach to recycle PV. Of the major subsystems, the EPS (energy/power subsystem) is the largest aside from the payload itself. It's also perhaps the most critical. Without power, your satellite is junk. The largest constituent of the EPS is the PV module. This is why PV is our main focus, and Lunexus was awarded an NSF Ph1 to further develop the gravity agnostic fluidized bed reactor at the heart of this. We completed that research and are currently awaiting word on the follow on Ph2 from the NSF.

In solving some of the basic problems for recycling and fabricating PV silicon, we are solving some of the ubiquitous problems of manufacturing anything in orbit. This moves everybody closer. We can't address all of the nodes ourself, but we might be able to help you, and you might be able to help us.

Who wants to make stuff happen?