Every serious ISAM business plan contains a section that goes something like this: "The space environment offers unique advantages — vacuum, microgravity, and abundant solar — that make in-space manufacturing compelling…" Then the slide moves on. Nobody does the math.

We're going to do the math. Or at least set up the framework for doing it properly, because the question of what vacuum and microgravity are actually worth (in dollars, not sentiment) is the foundational question for any manufacturing business case that depends on launch costs.

And launch costs matter. A lot. Whatever any industry report tells you about $2,700/kg Falcon 9 launch costs, the real number that commercial operators face is at least $3,500/kg. SpaceX's internal cost is lower; the market clearing price is not. Demand is outpacing both competition and launch technology, and basic economics dictates that prices are set by supply and demand. Demand is increasing faster than supply. Start every analysis there. Everything that follows has to pencil out against that.

METHOD: REVEALED PREFERENCE FROM PROXY SPENDING

The cleanest way to value an environment that doesn't yet have a mature commercial market is to look at what people actually spend to approximate that environment on Earth. This is revealed preference: what someone pays for a substitute is a floor on the value of the real thing. The gap between what the substitute delivers and what the orbital version provides is where the upside lives.

This framework applies differently to vacuum and microgravity. That difference turns out to be enormously consequential.

#1. MICROGRAVITY

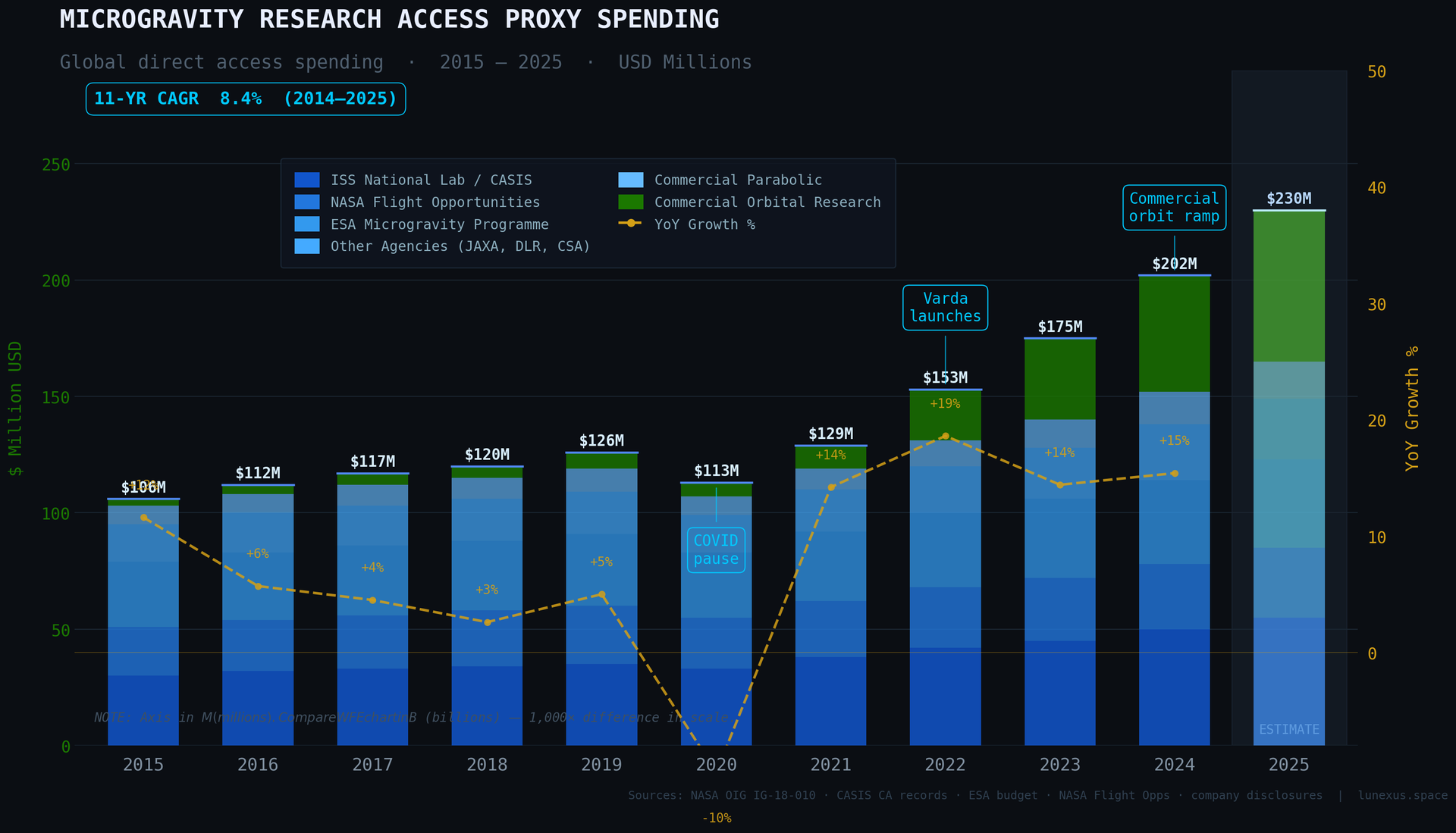

Let us first address microgravity, because that's what most fascinates the inner child with dreams of flight resident in us humans. Unfortunately,he proxy market for microgravity is almost as nascent as the actual market. The parts relevant to ISAM are driven by a combination of hope, hype, and curiosity, but we'll include also the parts used to qualify spaceward components for satellites. We will leave out the computer simulations (which we'll do for the vacuum comparison as well later). What's left are the various ways we have to create free-fall conditions:

| MICROGRAVITY ACCESS MECHANISM | DURATION | COST SIGNAL | WHO'S PAYING |

| ISS/CASIS research access (US) | Weeks–months | ~$4M/yr (NSF grants) | Government |

| ISS one-way payload transport | Indefinite | $80K–$90K per experiment | Government / Academic |

| Parabolic flight (Zero-G aircraft) | ~20 sec per parabola | ~$5K per person / flight | Academic / Some commercial |

| Drop tower (NASA Glenn) | 5 seconds | Low / gov-subsidized | Government / Academic |

| Suborbital (sounding rockets) | Minutes | $500K–$2M per flight | Government / Academic |

Sources: NSF/CASIS solicitation data; AIAA Aerospace America; ISS National Lab investment perspectives, 2024–2025.

The NSF-CASIS partnership (the primary external research funding mechanism for ISS microgravity access) has allocated roughly $40 million total over a decade. That's about $4 million a year. Global spending on microgravity access across all mechanisms is in the low hundreds of millions annually. Mostly government grants. Mostly basic research. No commercial manufacturing at meaningful scale.

The current microgravity market is paying for knowledge about microgravity, not for products made inmicrogravity. That's a critical distinction. ZBLAN fiber and space based biopharma together are estimated to be a combined $10-15B market, and their customers are on Earth, meaning every business case requires a full round-trip at $3,500/kg up and significant reentry costs down.

This doesn't mean microgravity is worthless. It means its value is currently speculative and unproven at scale.

#2. VACUUM

No, we aren't selling vacuum cleaners door to door here. The proxy we must target is process vacuum equipment for manufacturing: the systems that create and sustain high vacuum as a primary manufacturing input on Earth's surface.

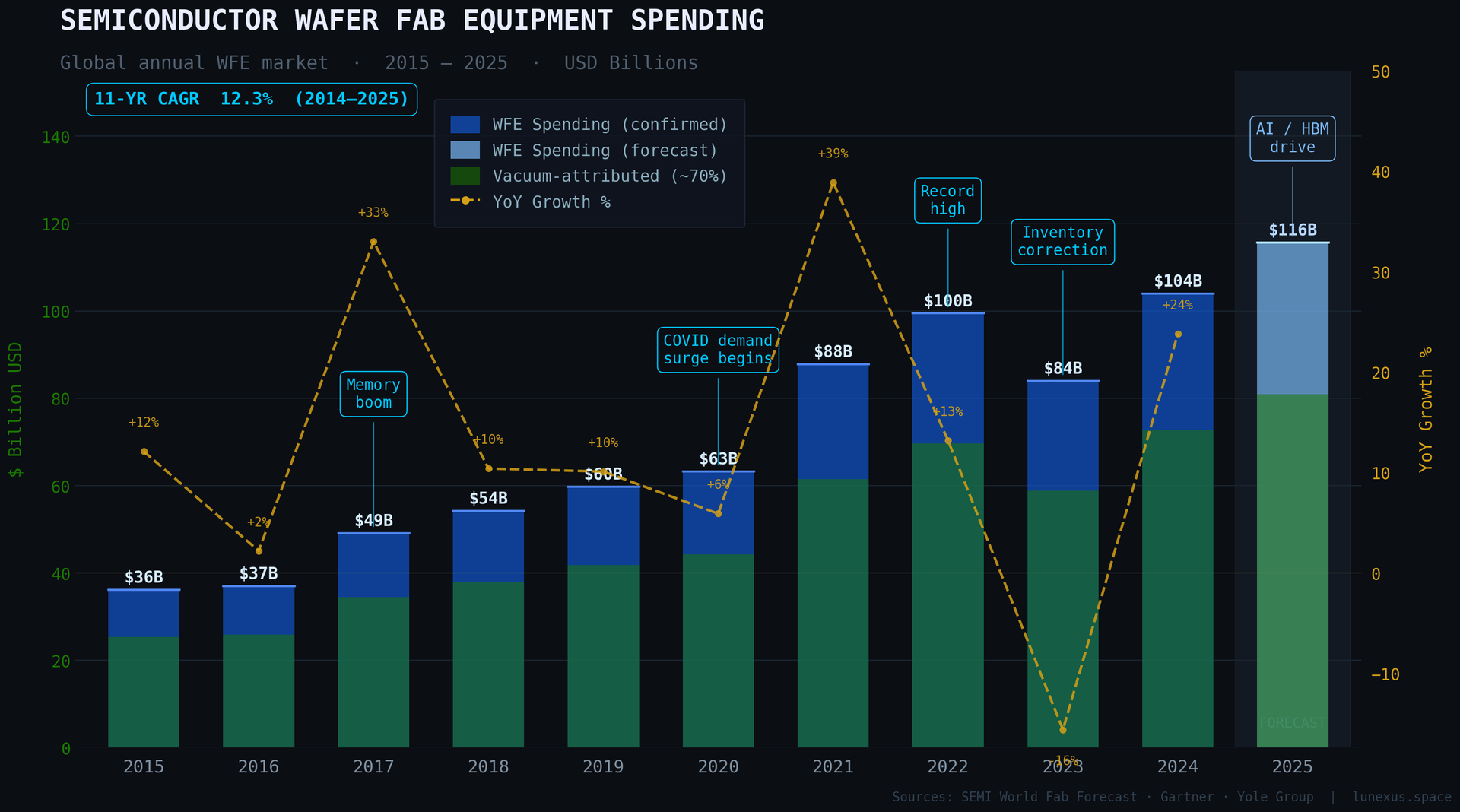

Every semiconductor goes through at least three vacuum chambers: crystal growth, doping, and photolithography. Vacuum is not optional for advanced semiconductors. It is the process environment. Global wafer fab equipment (WFE) spending — the annual bill for the tools that make this happen — hit $104 billion in 2024 and has compounded at roughly 12% annually for a decade.

Note that the vertical scale of this chart is in $B (rather than $M as the previous one was). However, not every dollar of fab equipment is vacuum-dependent. Wet etch, CMP, photoresist track, and cleaning tools are largely atmospheric. To get an honest signal for vacuum's value, you have to attribute WFE spending by process step.

Process-level attribution based on equipment category definitions. EUV lithography vacuum requirement drives the high fraction for that category; ASML machines require a vacuum path cleaner than outer space.

| WFE PROCESS CATEGORY | WFE SHARE | VACUUM-DEPENDENT FRACTION | VACUUM-ATTRIBUTED WFE |

| Deposition (CVD, PVD, ALD, Epi) | 25% | 100% | 25% |

| Etch (plasma/dry etch) | 20% | 88% | 18% |

| Lithography (EUV dominant at leading nodes) | 27% | 82% | 22% |

| Metrology & Inspection (e-beam, SEM) | 12% | 50% | ~6% |

| Thermal Diffusion, Doping | 5% | 40% | 2% |

| CMP, Wet Clean, Track | 10% | 5% | 0.5% |

| Total | 100% | 70-75% |

Sources: SEMI WFE category data, equipment vendor disclosures, 2024–2025.

So a defensible figure is that 70–75% of WFE is vacuum-dependent (meaning the process either requires high vacuum as the operating environment, or requires vacuum-quality pressure management as a core design constraint). At $104B in 2024 WFE, that's conservatively $73 billion annually spent on vacuum-dependent semiconductor manufacturing equipment, for front-end fab alone. In the WFE CapEx chart above, the vacuum portion is the green.

BUT WAIT, CAN'T WE JUST BUILD A CHAMBER ON EARTH?

Yes. And we do. That's exactly the point. The terrestrial vacuum equipment market exists because we can approximate orbital vacuum on Earth. The question is what it costs and what limitations we accept:

- Chamber size is a hard limit. Large-format crystal boules, extended fiber draws, and future structural components hit physical and economic pumpdown geometry limits. Bigger chambers cost exponentially more to build and operate.

- Pumpdown time is a throughput tax. Every cycle that requires venting and repumping burns time and energy. Orbital processing is continuous: no pump, no cycle, no wait.

- Qualification testing doubles the cost. All Earth-manufactured space hardware must be vacuum-tested before launch. Hardware manufactured in orbit never needs to be. It was born there.

Orbital vacuum is not just cheaper than a chamber at scale, it is operationally superior for continuous large-format processes. The terrestrial spending is a floor on value, not a ceiling.

THE 500:1 RATIO

$73 billion is annually spent on equipment whose sole purpose is to replicate, at great expense and in constrained geometry, an environment that exists for free in LEO. Compare this to global microgravity research access spending, estimated at $100–200M per year, almost entirely government-funded. The ratio is roughly 500:1. This is a revealed preference signal, not an opinion.

This asymmetry should discipline every ISAM business case. It doesn't mean microgravity has no future value. It means its value is currently unproven by market behavior, while vacuum's value is being demonstrated daily at enormous and growing scale on the ground. The WFE market has compounded at ~12% annually for a decade and shows no sign of decelerating.

A CLEAN VALUE HIERARCHY

When you run the proxy spending analysis honestly and layer in the $3,500/kg launch constraint, a cleaner product hierarchy emerges than most ISAM literature acknowledges:

TIER 1: IN-SPACE PRODUCTS

Semiconductors, PV cells, and structural components manufactured and used in orbit. No return cost. Customer is in the same environment as the factory. The satellite constellation market is doubling every two years — demand exists now, not eventually.

TIER 2: HIGH VALUE EARTH RETURN

Specialty substrates and seed crystals where price/gram can absorb $3,500/kg launch plus reentry costs. Extremely narrow product space. Requires demonstrated manufacturing yield at scale..

TIER 3: BULK / GENERIC MFG

Anything where the value per kg doesn't survive honest launch cost arithmetic. Structural metals, generic feedstocks, and most research applications without a sellable product.

Notice that Tier 1 doesn't depend on orbital data centers or speculative future demand. The satellite constellation build-out is already super-linear. Every Starlink, Kuiper, and regional broadband satellite launched is a customer for in-orbit semiconductor and PV manufacturing, if that manufacturing infrastructure existed. The demand is there. The factory isn't yet.

This connects directly to the hype curve concept. With this framework we can properly place technologies where they belong on the hype curve. We can use this to inform where we want to invest our money and effort. This isn't to say microgravity won't prove to be the killer app for ISAM, but there is an element of speculation and risk in that hype.

Of course, this is a very narrow look at the value of space as an environment. It completely neglects the real estate component, which is a topic for another post.